Should rising interest rates change your financial priorities?

What is a CLO?

An investor’s guide to marketplace lending

Beyond Mars, AeroVironment’s earthly expansion fueled by U.S. Bank

Housing market trends and relocation impact

Payment industry trends that are the future of POS

What are conforming loan limits and why are they increasing

What you need to know before buying a new or used car

Maximizing your infrastructure finance project with a full suite trustee and agent

8 steps to take before you buy a home

Evaluating interest rate risk creating risk management strategy

How to make the most of your business loan

5 tips for managing your business cash flow

Money Moments: How to finance a home addition

How Everyday Funding can improve cash flow

Staying organized when taking payments

How to fund your business without using 401(k) savings

What’s the difference between Fannie Mae and Freddie Mac?

4 benefits of independent loan agents

At your service: outsourcing loan agency work

Changes in credit reporting and what it means for homebuyers

How to accept credit cards online

Unexpected expenses: 5 small business costs to know and how to finance them

How to identify what technology is needed for your small business

Common small business banking questions, answered

How increased supply chain visibility can combat disruptors

How small business owners can budget for the holiday season

These small home improvement projects offer big returns on investment

Webinar: Mortgage basics: Finding the right home loan for you

8 Ways for small business owners to manage their cash flow

Dear Money Mentor: What is cash-out refinancing and is it right for you?

Can ABL options fuel your business — and keep it running?

How to get started creating your business plan

Collateral options for ABL: What’s eligible, what’s not?

ABL mythbusters: The truth about asset-based lending

3 signs it’s time for your business to switch banks

3 ways to secure purchasing power

4 small business trends that could change the way you work

Tips for realtors to help clients get their homeownership goals back on track

Are you ready to restart your federal student loan payments?

How to choose the right business checking account

Leverage credit wisely to plug business cash flow gaps

The essential business tips for tax deductions

Middle-market direct lending: Obstacles and opportunities

How this photography business persevered through tough times

How jumbo loans can help home buyers and your builder business

How to apply for a business credit card

Does your side business need a separate bank account?

Webinar: Leading through uncertainty: CFO Insights Executive Roundtable

Do you need a business equipment loan?

Strengthen your brand with modern POS technology

How to choose the right business savings account

5 questions business owners need to consider before taking out a loan

Prioritizing payroll during the COVID-19 pandemic

Meet your business credit card support team

How to establish your business credit score

5 tips to help you land a small business loan

7 uncommon recruiting strategies that you may not have tried yet

Business credit card support

Streamline operations with all-in-one small business financial support

How to establish your business credit score

What is needed to apply for an SBA loan

Technology strategies to complement your business plan

Opening a business on a budget during COVID-19

When to consider switching banks for your business

6 common financial mistakes made by dentists (and how to avoid them)

Business credit card 101

Do I need a credit card for my small business?

What kind of credit card does my small business need?

7 steps to keep your personal and business finances separate

Tech lifecycle refresh: A tale of two philosophies

Test your loan savvy

Webinar: Mortgage basics: What’s the difference between interest rate and annual percentage rate?

How do I prequalify for a mortgage?

Can you take advantage of the dead equity in your home?

Webinar: Mortgage basics: How much house can you afford?

Is a home equity line of credit (HELOC) right for you?

Webinar: Mortgage basics: 3 Key steps in the homebuying process

Webinar: Mortgage basics: Buying or renting – What’s right for you?

How to use your home equity to finance home improvements

Webinar: Mortgage basics: What is refinancing, and is it right for you?

Should you get a home equity loan or a home equity line of credit?

6 questions to ask before buying a new home

What is refinancing a mortgage?

What to know when buying a home with your significant other

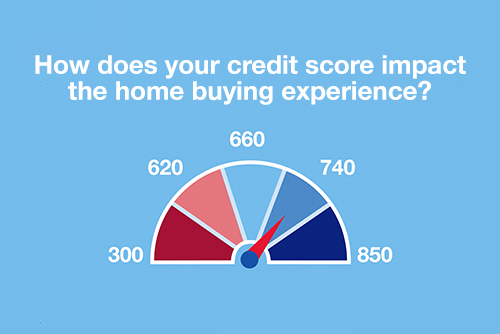

Webinar: Mortgage basics: How does your credit score impact the homebuying experience?

What is a home equity line of credit (HELOC) and what can it be used for?

Is it the right time to refinance your mortgage?

Overcoming high interest rates: Getting your homeownership goals back on track

Dear Money Mentor: How do I begin paying off credit card debt?

10 uses for a home equity loan

Is a home equity loan for college the right choice for your student

How to apply for federal student aid through the FAFSA

What to consider before taking out a student loan

Common unexpected expenses and three ways to pay for them

3 awkward situations Zelle can help avoid

How I did it: Paid off student loans

The A to Z’s of college loan terms

Costs to consider when starting a business

Questions to ask before buying a car

Webinar: Mortgage basics: Prequalification or pre-approval – What do I need?

Your financial aid guide: What are your options?

How you can take advantage of low mortgage rates

Personal loans first-timer's guide: 7 questions to ask

What you should know about buying a car

Take the stress out of buying your teen a car

How to choose the best car loan for you

Practical money skills and financial tips for college students

Co-signing 101: Applying for a loan with co-borrower

What’s a subordination agreement, and why does it matter?

Understanding the true cost of borrowing: What is amortization, and why does it matter?

What’s your financial IQ? Game-night edition

How to use debt to build wealth

How I did it: My house remodel

Everything you need to know about consolidating debts

Student checklist: Preparing for college

Webinar: Uncover the cost: College diploma

Your quick guide to loans and obtaining credit

Myths vs. facts about savings account interest rates

Break free from cash flow management constraints

4 questions to ask before you buy an investment property

How do interest rates affect investments?

Parent checklist: Preparing for college

Evaluating interest rate risk creating risk management strategy