What is a good credit score?

For small business growth, consider the international market

Refinancing your practice loans: What to know

What type of loan is right for your business?

Beyond Mars, AeroVironment’s earthly expansion fueled by U.S. Bank

How liquid asset secured financing helps with cash flow

Hybridization driving demand

Business risk management for owners of small companies

Digital banking and cloud accounting software: How they work together

Evaluating interest rate risk creating risk management strategy

How to make the most of your business loan

Money Moments: How to finance a home addition

Tech tools to keep your restaurant operations running smoothly

How to request a credit limit increase

How to fund your business without using 401(k) savings

Building a business with a great product and a greater purpose

Mapping out success for a small-business owner

Save time with mobile apps for business finances

How to identify what technology is needed for your small business

Tools that can streamline staffing and employee management

Honey Luxury Beauté: growing a side project into an eye-catching beauty business

Common small business banking questions, answered

How increased supply chain visibility can combat disruptors

How a family-owned newspaper is serving its community

Making the leap from employee to owner

How small business owners can budget for the holiday season

These small home improvement projects offer big returns on investment

In a digital world, Liberty Puzzles embraces true connection

8 Ways for small business owners to manage their cash flow

How to get started creating your business plan

3 signs it’s time for your business to switch banks

4 small business trends that could change the way you work

5 ways a business credit card program can grow your business

Why credit cards should be the first choice for business payments

5 tips to use your credit card wisely and steer clear of debt

How to build and maintain a solid credit history and score

How to improve your credit score

6 essential credit report terms to know

Leverage credit wisely to plug business cash flow gaps

How this photography business persevered through tough times

How to apply for a business credit card

Do you need a business equipment loan?

How to choose the right business savings account

5 questions business owners need to consider before taking out a loan

Prioritizing payroll during the COVID-19 pandemic

How to establish your business credit score

5 tips to help you land a small business loan

7 uncommon recruiting strategies that you may not have tried yet

Streamline operations with all-in-one small business financial support

Planning for restaurant startup costs and when to expect them

The moment I knew I’d made it: The Cheesecakery

How a bright idea became a successful business (in Charlotte, North Carolina)

How to establish your business credit score

What is needed to apply for an SBA loan

How a travel clothing retailer is staying true to its brand values

Opening a business on a budget during COVID-19

How to expand your business: Does a new location make sense?

How I did it: Grew my business by branching out

How small businesses are growing sales with online ordering

When small business and community work together

6 common financial mistakes made by dentists (and how to avoid them)

Business credit card 101

Do I need a credit card for my small business?

What kind of credit card does my small business need?

How a group fitness studio made the most of online workouts

Community and Coffee: How one small business owner is breaking down barriers

How community gave life to lifestyle boutique Les Sol

The San Francisco bridal shop that’s been making memories for 30 years

Community behind Elsa’s House of Sleep

How Wenonah Canoe is making a boom in business last

How Lip Esteem is empowering women

How running a business that aligns with core values is paying off

How Gentlemen Cuts helps its community shine

Meet the Milwaukee businessman behind Funky Fresh Spring Rolls

5 steps to selecting your first credit card

Credit: Do you understand it?

What types of credit scores qualify for a mortgage?

Can you take advantage of the dead equity in your home?

Webinar: Mortgage basics: How much house can you afford?

Is a home equity line of credit (HELOC) right for you?

How to use your home equity to finance home improvements

Should you get a home equity loan or a home equity line of credit?

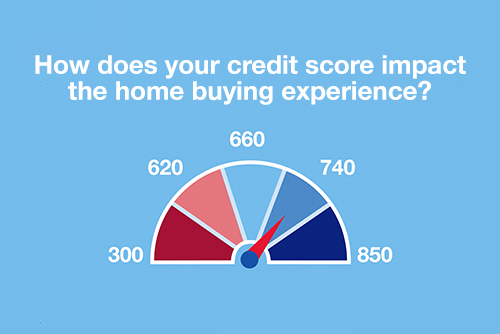

Webinar: Mortgage basics: How does your credit score impact the homebuying experience?

How to use credit cards wisely for a vacation budget

Dear Money Mentor: How do I begin paying off credit card debt?

10 uses for a home equity loan

Know your debt-to-income ratio

Common unexpected expenses and three ways to pay for them

How Shampoo’ed is transforming hair and inspiring entrepreneurs

Should you give your child a college credit card?

The different types of startup financing

Myth vs. truth: What affects your credit score?

Improving your credit score: Truth and myths revealed

Decoding credit: Understanding the 5 C’s

Making a ‘workout’ work out as a business

5 unique ways to take your credit card benefits further

5 tips to use your credit card wisely and steer clear of debt

What’s a subordination agreement, and why does it matter?

What’s your financial IQ? Game-night edition

How to build credit as a student

Celebrity Cake Studio’s two decades of growth and success

How Al’s Breakfast is bringing people together

Your quick guide to loans and obtaining credit

How tenacity brought Taste of Rondo to life

How a bar trivia company went digital during COVID-19

4 questions to ask before you buy an investment property

Good debt vs. bad debt: Know the difference

U.S. Bank asks: What do you know about credit?