What is a good credit score?

10 ways a global custodian can support your growth

Refinancing your practice loans: What to know

What type of loan is right for your business?

Beyond Mars, AeroVironment’s earthly expansion fueled by U.S. Bank

How liquid asset secured financing helps with cash flow

Hybridization driving demand

Evaluating interest rate risk creating risk management strategy

ePOS cash register training tips and tricks

How to make the most of your business loan

5 tips for managing your business cash flow

Money Moments: How to finance a home addition

A simple guide to set up your online ordering restaurant

Tech tools to keep your restaurant operations running smoothly

How Everyday Funding can improve cash flow

How to request a credit limit increase

4 ways Request for Payments (RfP) changes consumer bill pay

Cashless business pros and cons: Should you make the switch?

Higher education and the cashless society: Latest trends

How to fund your business without using 401(k) savings

Unexpected expenses: 5 small business costs to know and how to finance them

How to identify what technology is needed for your small business

Tools that can streamline staffing and employee management

Common small business banking questions, answered

These small home improvement projects offer big returns on investment

8 Ways for small business owners to manage their cash flow

How to get started creating your business plan

ABL mythbusters: The truth about asset-based lending

3 signs it’s time for your business to switch banks

4 small business trends that could change the way you work

5 tips to use your credit card wisely and steer clear of debt

How to build and maintain a solid credit history and score

How to improve your credit score

6 essential credit report terms to know

Leverage credit wisely to plug business cash flow gaps

What corporate treasurers need to know about Virtual Account Management

How jumbo loans can help home buyers and your builder business

How to apply for a business credit card

Do you need a business equipment loan?

How to choose the right business savings account

5 questions business owners need to consider before taking out a loan

Meet your business credit card support team

How to establish your business credit score

5 tips to help you land a small business loan

Streamline operations with all-in-one small business financial support

Planning for restaurant startup costs and when to expect them

The moment I knew I’d made it: The Cheesecakery

How to establish your business credit score

What is needed to apply for an SBA loan

Why retail merchandise returns will be a differentiator in 2022

How business owners are managing during the supply chain crisis

Technology strategies to complement your business plan

How to expand your business: Does a new location make sense?

How small businesses are growing sales with online ordering

6 common financial mistakes made by dentists (and how to avoid them)

Business credit card 101

5 steps to selecting your first credit card

Credit: Do you understand it?

What types of credit scores qualify for a mortgage?

Can you take advantage of the dead equity in your home?

Webinar: Mortgage basics: How much house can you afford?

Is a home equity line of credit (HELOC) right for you?

How to use your home equity to finance home improvements

Should you get a home equity loan or a home equity line of credit?

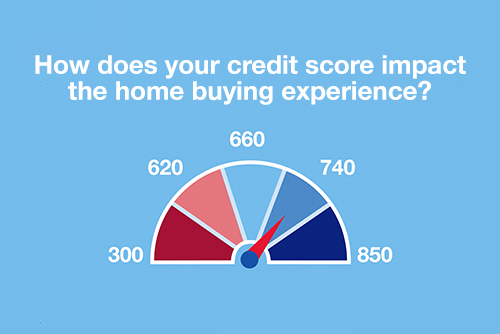

Webinar: Mortgage basics: How does your credit score impact the homebuying experience?

How to use credit cards wisely for a vacation budget

Dear Money Mentor: How do I begin paying off credit card debt?

10 uses for a home equity loan

Know your debt-to-income ratio

Common unexpected expenses and three ways to pay for them

Should you give your child a college credit card?

The different types of startup financing

Myth vs. truth: What affects your credit score?

Improving your credit score: Truth and myths revealed

Decoding credit: Understanding the 5 C’s

Dear Money Mentor: How do I set and track financial goals?

5 unique ways to take your credit card benefits further

5 tips to use your credit card wisely and steer clear of debt

What’s a subordination agreement, and why does it matter?

What’s your financial IQ? Game-night edition

How to build credit as a student

30-day adulting challenge: Financial wellness tasks to complete in a month

Your quick guide to loans and obtaining credit

Break free from cash flow management constraints

4 questions to ask before you buy an investment property

Good debt vs. bad debt: Know the difference

U.S. Bank asks: What do you know about credit?

Evaluating interest rate risk creating risk management strategy