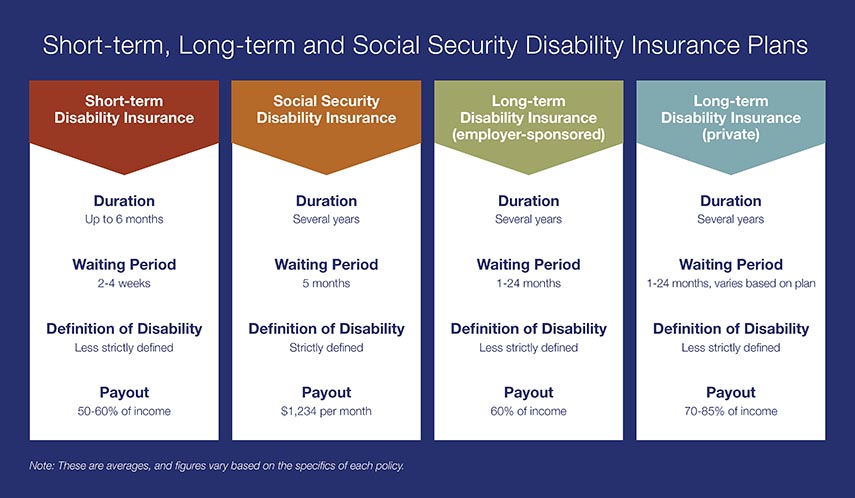

Life insurance can offer financial coverage and security to your loved ones, but it can be hard to know how much you need to purchase.

Life insurance isn’t just about preparing for life’s worst-case scenarios. It can and should play an active role in your overall financial plan.

However, how much life insurance you need isn’t a one-size-fits-all answer. It will depend on a variety of factors, including your age, your family situation, your reasons for buying a policy, and your financial goals. Even more, many of these will change over the course of your life.

Here are some insights to help determine the type and amount of life insurance you might need.

Life insurance for income replacement

One of the most common reasons for purchasing life insurance is to replace future income that would be lost if you should die prematurely. The goal is to make sure your family can maintain the same standard of living over certain amount of time, as well as support other financial goals such as a college education for children and retirement saving.

Typically, term life insurance is the most affordable and practical alternative to consider. Term insurance is designed to pay death benefits only if the insured individual dies during the span of time covered by the policy.

How much term life insurance is enough to provide the appropriate level of protection for your family? Here are some guidelines:

- A general rule of thumb is to buy a policy worth 8 to 10 times an individual’s annual income. For example, if your annual salary is $100,000, it makes sense to consider a policy with a $1 million death benefit.

- Consider not just your income today, but how it may grow over time. If you make $100,000 a year today, you may earn $150,000/year in 5 to 10 years. You should account for that potential change.

- Factor in the specific circumstances of your family, including the age of your children, whether you plan to have more, and what your spouse earns. If you have a young family, you might want a policy that lasts 20 or 30 years.

- Think about the time-value of money and how inflation will decrease the value of the benefits over time.

- Keep in mind that life insurance proceeds generally aren’t taxable, so you can factor in “after-tax” income needs as you project the required coverage.

Given the relatively low cost of term insurance, it may make sense to have more coverage than you think you need.

Options for purchasing term life policies

Once you’ve determined your coverage needs, you need to decide whether it makes sense to own one large policy or multiple policies.

Owning a single policy makes the process simpler. If you work with a single insurance provider, you only need to go through the underwriting process once. It makes managing payments easier as well.

However, you may find “laddering” insurance policies provides you the full level of coverage you need. This means purchasing several term insurance policies covering different time spans. After all, if you determine you need $1 million of coverage today, you won’t need that much to meet needs 10 or 20 years from now.

As an example, if you’re 40 and looking to protect your spouse and three children, you may want to ladder:

- A 10-year policy to provide coverage for when household expenses will be higher.

- A 20-year policy to help meet additional costs related to sending the children to college.

- A 25- or 30-year policy to ensure a stream of income is available for the surviving spouse.

Typically, the shorter the policy term, the less costly insurance is on an annual basis. Therefore, a laddering approach can be a more cost-effective way to structure a long-term income replacement plan.

Life insurance to protect late-in-life risks

Life insurance needs change over time. As you grow older, you’ll most likely worry less about your ability to support your family monetarily and worry more about the financial costs of your own potential long-term care. It’s estimated that even a healthy 65-year-old couple will have a 70% chance that at least one will require some sort of extended care during their retirement years.1

The good news is that many permanent life insurance policies also have a rider offering the flexibility to provide coverage for long-term care (LTC). Permanent life insurance is designed to last throughout your life and provide a death benefit to beneficiaries upon your passing. If you choose such a policy with an LTC rider, benefits can be paid to meet LTC expenses. If the policy is not tapped for that purpose during your lifetime, the full death benefit is paid out to beneficiaries.

The amount of coverage needed for a life insurance policy with an LTC rider varies from person to person, but it typically ranges between $500,000 and $750,000.

Estate planning with life insurance

Life insurance can also be used to provide an inheritance. For example, if you have three children, you might want each of them to receive $500,000. In that case, you’d want a permanent life insurance policy with a $1.5 million death benefit. Life insurance proceeds are generally not subject to income tax.

In addition, life insurance can play an important role in providing liquidity for larger estates that may be subject to estate taxation. In 2024, an individual can leave $13.61 million to heirs without paying federal estate or gift tax. However, if assets above that limit are illiquid, such as a farm, business or other real estate, families may have to sell these assets to pay the tax, which could at a rate as high as 40%.

A permanent life insurance policy with death benefits that cover projected estate taxes can give beneficiaries the liquidity they need to preserve the estate.

Business continuity planning with life insurance

If you own or co-own a business, you may want to consider buying a life insurance policy on your business partner as part of your business succession planning. You should also consider purchasing key person life insurance for employees your business is particularly dependent on. This helps create cash flow for the business to continue to function in the case of an unexpected event such as death or disability.

Many businesses with co-owners utilize life insurance in the form of a buy-sell agreement that states that the surviving partner can buy out the heirs of a deceased partner. For example, if you and a partner each own 50% of a business worth $5 million, you’d want a life insurance policy with a $2.5 million death benefit. Make sure you get a fair-value assessment of the business before buying a policy.

Answering the question of “how much life insurance do I need” is an important part of your financial planning process. Determining the proper amount of insurance to carry is a complex matter. A financial advisor can help you assess your life insurance needs and choices.

Learn more about the role life insurance can play in your financial plan.